A Guide to Check Fraud Prevention

When was the last time you looked closely at a check? Think for a moment about all the information it contains: your full name, your address, your routing number, your bank account number, and your signature. Now, imagine all that information falling into the hands of a thief.

This isn’t paranoia – it’s the reality of check fraud. Paper checks, while convenient, are vulnerable to theft and alteration, making them a prime target for fraudsters.

Check fraud is more common than you might think and can leave you (or your business) with significant financial loss and headaches. Check fraud is a widespread problem affecting hundreds of thousands of people every year, with losses in the millions.

We often don’t consider the vulnerability of a simple paper check, but in the wrong hands, it can lead to counterfeit schemes, forged signatures, and worse. A stolen check can not only drain your bank account, but also expose your personal information, leading to identity theft.

Read on to arm yourself with the knowledge to safeguard your checks—and your identity.

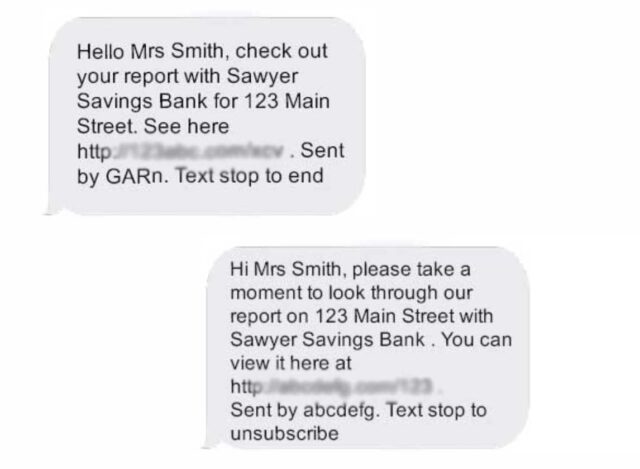

The Dangers of Mailing Your Checks

Even in our digital world, the humble paper check remains a staple of personal and business transactions. But this means of transferring funds comes with significant risks, especially given the advances in fraudulent techniques.

Unsecured mailboxes are easy targets for thieves to steal your check. A paper check can be “washed” and rendered blank, an alteration made, and the payee modified without your knowledge. Checks can be snatched and quickly altered using simple chemicals and cashed in by someone entirely different than the intended recipient. However, there are several ways to protect yourself from fraud.

Understanding the Types of Check Fraud

Fraudsters have various ploys when it comes to checks. They may set up counterfeit check scams, forge signatures, alter checks to change payee names or amounts, or, most alarmingly, take over your entire bank account. These frauds aren’t just financial crimes; they often lead to headaches like liability disputes and damaged credit.

Here are some common types to be aware of:

- Counterfeit Checks: Fraudsters create fake checks that resemble legitimate ones.

- Forged Signatures: Thieves steal your check and forge your signature to cash it.

- Alterations (Washing): Criminals use chemicals to remove the original payee and amount information on a check, then rewrite it with their own details.

- Account Takeover: Hackers gain access to your bank account information to write and cash fraudulent checks electronically.

The Best Defense is a Good Offense

It’s essential to be cautious in your financial dealings, especially those involving checks. With check fraud, prevention is key. There are simple, proactive measures you can take to protect yourself or your business from these financial landmines.

Pen Power and Secure Writing

It may sound like something out of a spy movie, but the type of pen you use to write checks matters. Opt for black gel pens for enhanced protection. The type of pigments used in gel pens seep into the fibers of the check, making it much harder to “wash.”

Ensuring Safe Mailing and Monitoring

Deposit checks as close to mail collection times as possible, or better yet, directly at the post office, to minimize the window of opportunity for theft. By timing your check deposits to coincide with mail collection times and regularly checking bank statements, you can drastically reduce the chances of fraudsters getting hold of your checks.

Record Keeping and Fast Action

Maintain a record of all issued checks (payee, amount, date), and closely monitor your bank statements or online banking activity for cleared checks. Look for discrepancies and utilize check images when available to verify payee information hasn’t been altered.

If you suspect check fraud, contact us immediately to report the incident and take steps to secure your account.

Make the Switch to Electronic Payments

Whenever possible, skip the check entirely and make an electronic payment. Many businesses offer online bill payment options, and for sending money to friends and family, consider a peer-to-peer (P2P) payment service. Online bill payments and electronic transfers offer a high level of security, significantly reducing the risk of fraud that comes with paper checks.

Stop Fraud with Safer Strategies in Your Financial Security

Implementing these practices is relatively simple and can save you a significant amount of money and stress. Take control of your financial security by being vigilant and purposeful in the way you handle paper checks.

There are additional steps you can take, in business and at home, to minimize the risk of check fraud even when you aren’t actively writing paper checks.

- Be Wary of Personal Information Sharing: Don’t readily share your bank account details or write checks to unknown parties.

- Monitor Your Statements: Regularly review your bank statements (online or paper) to identify any discrepancies or unauthorized transactions.

- Beware of Unsolicited Checks: Be cautious of offers to receive unsolicited checks, especially if they require you to send money back. These could be scams.

- Dual Control for Businesses: Businesses and freelancers should implement dual control procedures for check writing, requiring two authorized signatures before issuing a check.

- Regular Audits: Conduct regular internal audits to identify potential vulnerabilities in your check-writing process.

- Invest in Security: Consider using secure check printing technologies that make checks more difficult to alter.

Don’t Let Your Rent Check Become Someone Else’s Payday

Remember, while checks are a useful method of payment, they aren’t without risks. Combining electronic payment options with the safety measures outlined above can significantly reduce the risk of check fraud.

To recap, that means:

- prioritize electronic payments whenever possible,

- use gel pens when writing checks,

- be mindful of mailing times,

- and diligently monitor your bank statements.

Taking these steps empowers you to protect your hard-earned money and safeguard yourself from the growing threat of check fraud. It’s an investment in peace of mind that is well worth the effort.